London, UK – 13 November 2025 — Latest data from the Office for National Statistics (ONS) reveal that the UK Economy expanded by just 0.1 % in Q3 2025, down from 0.3 % in the previous quarter and below market expectations of 0.2 %.

The unusually weak result reflects a combination of external shocks and structural headwinds, including a major cyber-attack on Jaguar Land Rover (JLR) that disrupted UK motor manufacturing and significantly dampened output in September, which alone fell by 0.1 %.

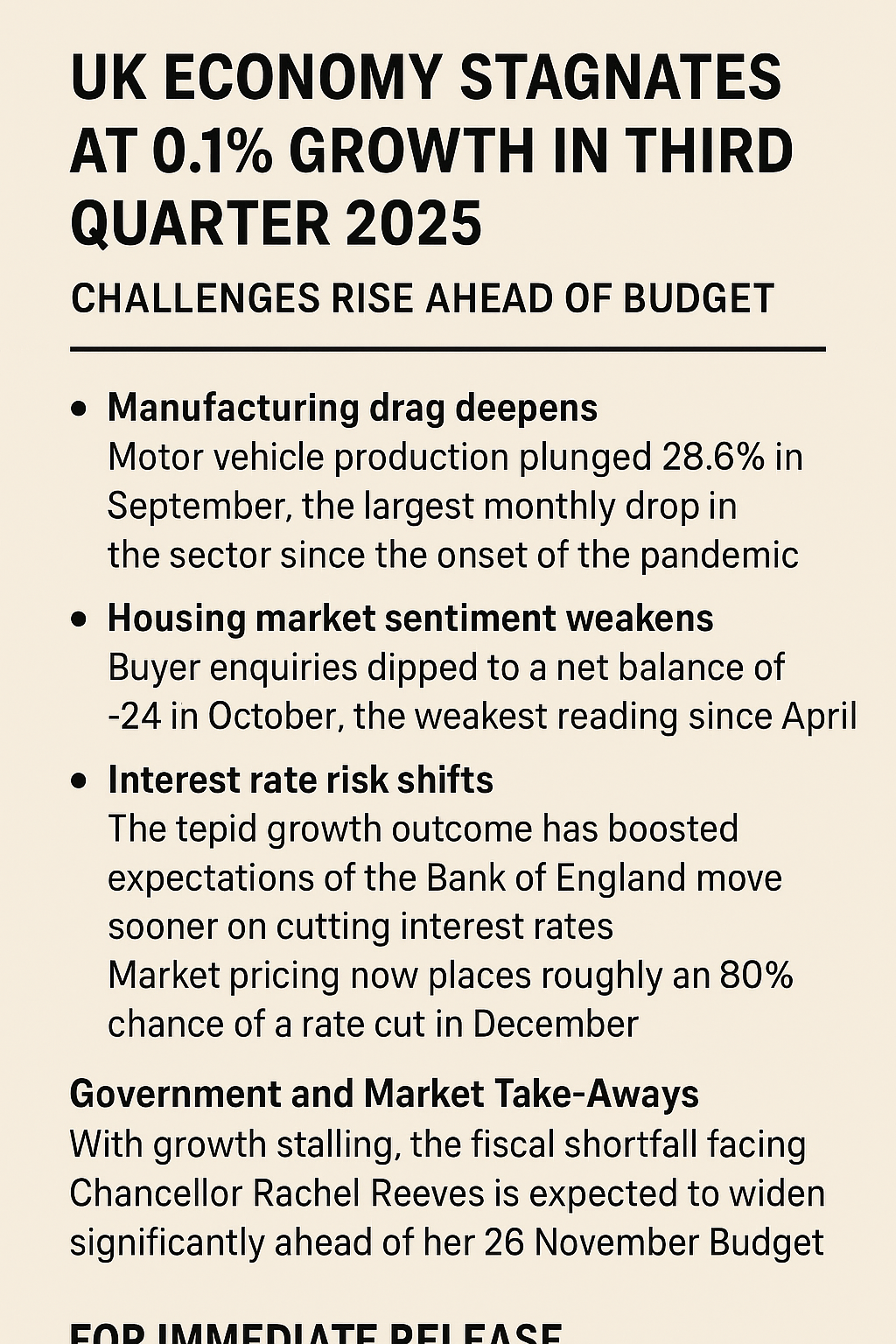

Key Findings & Market Impacts

• Manufacturing drag deepens

Motor vehicle production plunged 28.6 % in September— the largest monthly drop in the sector since the onset of the pandemic. The attack on JLR, which halted production in multiple plants, was central. Reuters+1

The contraction in goods output contributed to overall GDP growth being nearly flat for the quarter.

• Housing market sentiment weakens

According to the Royal Institution of Chartered Surveyors (RICS), buyer enquiries in the UK housing market dipped to a net balance of -24 in October (from -21 in September), the weakest reading since April. House price sentiment also weakened to -19.

The slowdown reflects mounting consumer caution ahead of the upcoming Budget and concerns about tax changes.

• Interest rate risk shifts

The tepid growth outcome has boosted expectations that the Bank of England might move sooner on cutting interest rates. Market pricing now places roughly an 80 % chance of a rate cut in December.

Government and Market Take-Aways

Fiscal Pressure Increases. With growth stalling, the fiscal shortfall facing Chancellor Rachel Reeves is expected to widen significantly ahead of her 26 November Budget. Tax rises, spending restraint or a combination of both appear increasingly probable.

Investor caution mounts. Institutional investors and market watchers are revising their UK outlook amid lower growth and policy uncertainty:

- Risk premium on UK assets may rise.

- Corporate investment decisions could be delayed.

- Sterling may come under pressure if global growth dampens.

Opportunities emerge. For firms and investors that can act quickly:

- Lower interest rates or liquidity injections could trigger a rebound in sectors sensitive to funding costs.

- Housing-market weakness may offer buying opportunities in property-related stocks or REITs.

- Companies with strong export or tech exposure may stand out amid domestic weakness.

Looking Ahead

In the near term, attention will focus on:

- The Chancellor’s Budget (26 November) and how it addresses the fiscal gap and growth shortfall.

- Q4 GDP data and early signals of whether the drag from manufacturing eases.

- Bank of England commentary and decisions on the interest-rate path.

- Corporate earnings as firms adapt to softer demand and a challenging economic backdrop.

About

[] is a London-based financial research and advisory firm specialising in macro-economic analysis, quantitative trading insights and institutional research across equities, fixed income and digital assets.

Media Contact:

FalconEdge Analytics Ltd

Location: London, United Kingdom

Email:media@falconedgeanalytics.co.uk

Phone: +44 (0)20 3800 9271